A guide to gifting and Inheritance Tax

One of the most valuable strategies we recommend to clients is financial gifting.

Used wisely, gifting can reduce your estate’s IHT liability while helping loved ones in a meaningful way during your lifetime.

In this guide, we will explore the current UK gifting allowances, how to use them effectively, and common pitfalls to avoid.

Why consider gifting?

Gifting is a legitimate and effective way to reduce your estate’s value, potentially lowering or even eliminating a future IHT bill. Gifting can also help with:

- Supporting family members (e.g. helping children with housing costs)

- Passing on wealth during your lifetime

- Avoiding delays caused by probate

However, there are specific rules and thresholds that must be followed to ensure your gifts are tax-efficient and compliant.

Overview of UK gifting rules (2024/25)

Normal expenditure out of income – no limit

There is no cap on gifts made from surplus income, provided:

- The payments are regular

- They come from your normal income (e.g. salary, pension)

- You maintain your usual standard of living

Examples:

- Paying a grandchild’s rent or mobile bill

- Covering life insurance premiums

- Making regular contributions to a family member’s utility costs

This is a powerful and underused exemption for wealth transfer.

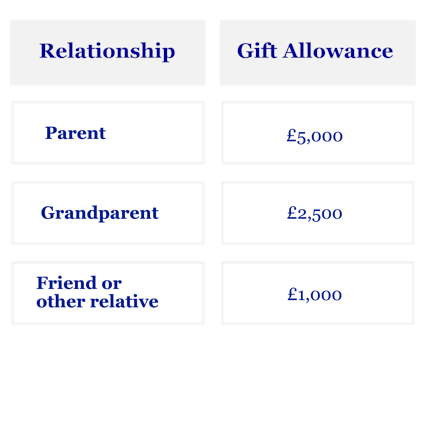

Wedding or civil partnership gifts – tax-free limits

If someone you know is getting married or entering a civil partnership, you can give them a tax-free gift based on your relationship:

Gifts must be made before the ceremony and won’t count against your annual exemption.

Annual exemption – £3,000

Each tax year, you can give away up to £3,000 IHT-free. If unused, the previous year’s allowance can be carried forward, letting you gift up to £6,000 in a single year.

This can be split among any number of recipients, but cannot be used in conjunction with the small gifts exemption (below) to the same person.

Small gifts exemption – £250 Per Person

You can also gift up to £250 per person per tax year, to any number of individuals, provided they haven’t also received part of your £3,000 annual exemption.

Gifts to spouses, civil partners, and charities

Here are the IHT-free limits for each category of recipient.

Potentially Exempt Transfers (PETs)

Larger one-off gifts to individuals, and gifts to absolute trusts are classed as Potentially Exempt Transfers.

- If you survive seven years after the gift, it becomes fully IHT-free.

- If you die within seven years, the gift may be subject to IHT, depending on its value and how long ago it was made.

How does taper relief work?

Taper relief reduces the tax payable on PETs over time:

Chargeable Lifetime Transfers (CLTs)

If a gift does not qualify as a PET, typically because it’s made to a discretionary trust, it becomes a Chargeable Lifetime Transfer.

- Subject to 20% IHT immediately on amounts over the nil-rate band (£325,000)

- May face further IHT if the donor dies within 7 years

Professional advice is essential when gifting to trusts, as rules are complex and the consequences significant.

Gifts with reservation

Be cautious: if you give away an asset but retain a benefit from it (e.g. continue living in a house you’ve gifted), it’s classed as a gift with reservation and may still be counted in your estate for IHT purposes.

Examples:

- Gifting your home but living there rent-free

- Giving away a car but still using it

- Donating art while keeping it displayed in your home

These arrangements can trigger full IHT on the asset’s value so must be planned carefully.

Get in touch for professional advice

Gifting can be an effective part of your estate planning strategy, but it needs to be done with care. Not all gifts are treated equally under UK tax law, and missteps can lead to unnecessary tax exposure.

At The Penny Group, we can help you to:

- Identify the most efficient gifting strategy for your goals

- Make full use of available exemptions

- Ensure you remain compliant with HMRC rules

With the upcoming changes to pension treatment and increased IHT exposure, now is a good time to act.

Remember, all decisions should be considered in the context of your own personal circumstances.

If you wish to discuss your financial position and the options available to you, please contact one of our advisers.

You can reach us at info@thepennygroup.co.uk or on 0207 061 2345.

HM Revenue and Customs practice and the law relating to taxation are complex and subject to individual circumstances and changes which cannot be foreseen.

Approved by The Openwork Partnership on 17/07/2025